Buying a car is more than just picking out your favorite model or deciding between leather or cloth seats—it’s a major financial move that can impact your budget for years to come. Whether you’re eyeing a brand-new vehicle straight off the lot or a dependable used car to get you from A to B, the price tag can be intimidating. And unless you have enough cash saved up to cover the full cost of the vehicle upfront (which most people don’t), you’ll likely need to consider car financing.

Car financing is one of the most common ways people pay for vehicles today. It allows you to take ownership of a car without having to pay the entire amount all at once. Instead, you borrow the money from a lender—like a bank, credit union, dealership, or online financing company—and repay it over time through monthly installments. This approach makes owning a car more accessible, especially when you’re trying to manage other financial responsibilities like rent, bills, or family expenses.

But as straightforward as it sounds, financing involves more than just signing some paperwork and driving off the lot. Interest rates, loan terms, credit scores, and down payments all play a role in shaping how much you’ll pay in the long run. And depending on how well you understand the process, financing can either work in your favor or end up costing you more than you expected.

So what exactly does car financing involve? How do you get approved? What factors influence your monthly payment? And how can you make sure you’re getting the best possible deal?

In this guide, we’ll walk you through the ins and outs of car financing—from what it is, to how it works, to the different options available. Whether you’re a first-time buyer or someone looking to brush up on the basics before your next purchase, this article will help you make confident, informed decisions when it comes to financing your next vehicle.

Table of contents

Understanding Car Financing

Car financing is a way to make vehicle ownership more accessible, especially when paying the full price of a car in cash isn’t practical. At its simplest, it means borrowing money from a lender to cover the cost of the vehicle, then repaying that amount gradually over time—usually with added interest. It turns what would be a large, upfront expense into a series of smaller, more manageable monthly payments.

Instead of needing $25,000 or more on hand to buy a car outright, financing lets you break that total down into payments spread across several years. Most auto loans range from 36 to 72 months, though some lenders offer even longer terms. While spreading out the cost can make ownership more affordable in the short term, it’s important to remember that you’ll also pay interest, which is essentially the cost of borrowing the money.

The interest rate you receive depends on a few things—most importantly, your credit score, income, loan term, and the lender’s own policies. A lower interest rate means you’ll pay less over time, while a higher rate can significantly increase the total cost of the loan. That’s why understanding financing—and preparing for it—is so important before you start shopping for a car.

When it comes to where to get a loan, you’ve got options. Many people choose to go through their bank or credit union, especially if they already have a good relationship there. These institutions often offer competitive rates and may be more flexible if you’re an existing customer. Others prefer the convenience of financing through the dealership. This typically involves working with a finance manager who submits your application to a variety of lenders—or, in some cases, the dealership may offer their own in-house financing, especially for certified pre-owned or promotional deals.

There’s also a growing number of online lenders that specialize in auto loans. These platforms let you compare rates from multiple lenders without leaving your home, and they often provide fast pre-approvals so you know what you can afford before visiting a dealership.

No matter which route you take, the goal of car financing is the same: to make buying a vehicle financially manageable. Instead of waiting years to save enough cash, financing allows you to get behind the wheel sooner—while paying for the car in a way that aligns with your monthly budget. It’s a tool that, when used wisely, can help you drive the car you need without putting your finances in a bind.

How the Process Works

Applying for car financing might seem intimidating at first, but once you understand the steps, it becomes much more approachable. Whether you’re working with a bank, credit union, online lender, or a dealership, the process usually follows a fairly standard path—with a few important decisions along the way.

It all starts when you submit a loan application. This can be done online, in person at a bank, or directly at the dealership. The lender will ask for personal and financial details, including your name, income, employment history, housing situation, and permission to pull your credit report. These details help them assess your overall financial health and determine how risky it would be to lend you money.

Once your application is submitted, the lender will review several key factors. Your credit score is often the most influential piece—lenders use it to predict how likely you are to repay the loan on time. But it’s not the only thing that matters. They’ll also look at your monthly income, how stable your employment is, and how much other debt you’re currently carrying. Together, these factors help lenders calculate your debt-to-income ratio—a key indicator of whether you can realistically afford new monthly payments.

If you meet their requirements, the lender will issue a loan offer. This will include a few important pieces: the amount you’re approved to borrow, your interest rate, the length of the loan term (usually expressed in months), and your estimated monthly payment. You can review these terms and decide whether to accept, negotiate, or explore other options.

At this point, you’ll also be expected to make a down payment. This is an upfront contribution toward the purchase price of the car. While down payments aren’t always required, putting money down is generally a smart move. Not only does it reduce the total amount you need to finance, but it can also help you qualify for better loan terms and lower your monthly payments. In the eyes of the lender, a strong down payment shows that you’re financially committed and capable of handling the loan.

Once the down payment is made and you accept the loan offer, the final paperwork is signed, and the lender sends the funds to the seller—whether that’s a dealership or private party. From there, you drive off in your new (or new-to-you) car, and begin making monthly payments based on your loan terms.

Throughout the life of the loan, it’s crucial to stay on top of those payments. Doing so not only keeps you in good standing but also helps build a positive credit history over time. Missing payments, on the other hand, can hurt your credit and potentially lead to repossession.

So, while the financing process might seem like a lot on the surface, it’s really just about preparation and understanding what each step involves. With the right approach and a bit of planning, you can walk into the process with confidence—and drive away with a deal that works for your budget and your goals.

Financing Options You Might Encounter

When it comes to buying a car, financing isn’t a one-size-fits-all experience. In fact, there are several different ways to secure a car loan, each with its own process, advantages, and potential drawbacks. The option you choose can have a big impact on how much you pay, how quickly you’re approved, and how flexible your loan terms are.

One of the most common routes is called direct lending. This is when you go straight to a bank, credit union, or online lender to get pre-approved for an auto loan before you even start shopping for a car. With direct lending, you get a clear picture of your budget up front, including how much you’re approved to borrow, what your interest rate will be, and what your monthly payments might look like. One major benefit here is control—you can take your pre-approval to any dealership and negotiate the price of the car without feeling pressured to use their financing. It also gives you the freedom to compare rates from multiple lenders and choose the most competitive offer.

Another common path is dealer financing, which is arranged directly through the dealership where you’re buying the car. In this scenario, the dealer acts as the middleman between you and the lender. They often work with a network of banks, finance companies, or even offer their own in-house financing. This can be incredibly convenient—especially if you’re eager to wrap everything up in one place. You can test-drive a car, negotiate the price, and handle the loan application all under the same roof.

Dealer financing can also come with special promotions, like low-interest deals or cashback offers, especially if you’re purchasing a new car from a major brand. However, it’s important to be cautious. Some dealers might mark up interest rates slightly to earn a commission from the loan, which means you could end up paying more over time than if you’d secured financing on your own.

There’s also a third option known as “buy here, pay here” financing, often offered by used car dealerships. These are usually geared toward buyers with bad or limited credit. The dealer provides the loan themselves, and you make payments directly to them. While it’s accessible and fast, this type of financing often comes with higher interest rates and less favorable terms. It can be a last-resort option, so it’s worth exploring others first if possible.

Ultimately, the right financing option depends on your personal situation—your credit, your budget, and how much time and effort you’re willing to put into shopping around. If you’re confident and want the best rate, direct lending may be the way to go. If you prefer convenience and a streamlined buying process, dealer financing might suit you better. And if you’re rebuilding credit, alternative financing could be a short-term solution—just be sure to read the fine print and understand what you’re signing up for.

Taking the time to understand these options can help you feel more in control and confident when it’s time to close the deal.

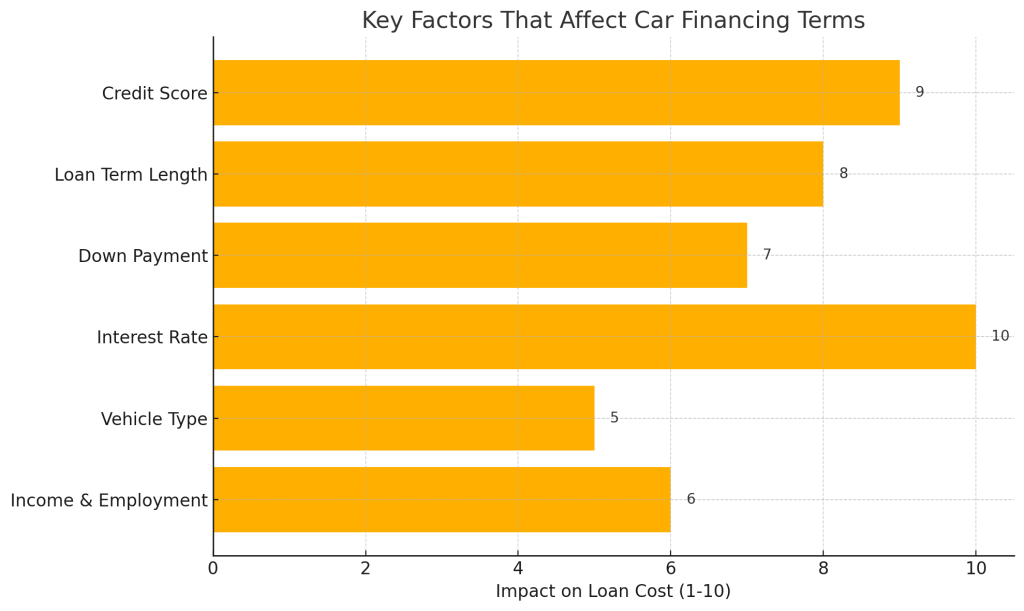

What Affects Your Financing Terms

When it comes to car financing, not all loan offers are created equal. The terms you’re offered—like your interest rate, monthly payment, and loan duration—can vary significantly based on several key factors. Understanding what influences these terms can help you make smarter decisions and potentially save a lot of money over time.

One of the biggest factors is your credit score. Lenders use it to gauge how risky it might be to lend you money. A higher credit score usually signals that you’ve managed debt responsibly in the past, so lenders reward you with lower interest rates. That lower rate can make a big difference—not just on your monthly payments, but on the total amount you’ll pay over the life of the loan. For example, a buyer with excellent credit might qualify for a rate below 5%, while someone with poor credit could be offered something closer to 10% or more.

But your credit score isn’t the only thing lenders look at. They also consider your down payment—how much money you’re able to put down upfront. The more you can pay right away, the less you’ll need to borrow, and the less risk the lender takes on. That can work in your favor when it comes to securing better loan terms. A larger down payment can also reduce your monthly payments and lower your chances of ending up “underwater” on your loan (where you owe more than the car is worth).

Another important factor is the vehicle itself. Lenders may offer more favorable terms for new cars compared to used ones, because new vehicles are generally considered less risky and more reliable. That said, new cars depreciate quickly, so it’s still wise to look at the full picture—especially if you’re considering a long loan term.

Speaking of which, the length of your loan matters, too. Shorter loan terms—like three or four years—typically come with higher monthly payments, but you’ll pay significantly less in interest overall. Longer terms, such as six or seven years, can make the monthly cost more manageable, but they often come with higher interest rates and increase the total amount you’ll repay. Plus, longer loans can leave you paying for a car long after its value has dropped.

Other personal details also come into play, such as your income, employment history, debt-to-income ratio, and even your ability to provide proof of stable housing. Lenders want to be confident that you can afford the loan and will pay it back on time.

In short, your financing terms depend on a mix of your financial history, the car you’re buying, and the structure of the loan itself. By improving your credit, saving for a bigger down payment, and choosing a loan term that balances affordability with financial efficiency, you can position yourself to get the best possible deal.

Is Financing the Right Choice for You?

Car financing can absolutely be a smart move—especially if you’re not ready to part with a large sum of money upfront. For many people, it’s the most practical way to afford a reliable vehicle without draining their savings or emergency funds. Instead of paying the full price of a car all at once, financing allows you to spread the cost over time through manageable monthly payments. This can make higher-quality vehicles more accessible and leave room in your budget for other important expenses.

Another benefit? Financing a car responsibly can actually help you build or improve your credit score. As long as you make your payments on time and in full, a car loan can demonstrate to future lenders that you’re a reliable borrower. Over time, this can lead to better interest rates—not just on cars, but on credit cards, mortgages, and other loans.

However, financing isn’t without its downsides. When you take out a loan, you agree to pay back not only the price of the car but also interest on the amount borrowed. Depending on your credit profile and loan terms, this can add up significantly over the life of the loan—sometimes thousands of dollars more than the vehicle’s original price. And while monthly payments might seem affordable at first, they can become a burden if your financial situation changes down the road.

There’s also the risk of owing more than your car is worth, especially if the car depreciates faster than you’re paying down the loan. This situation, known as being “upside down” on your loan, can make it difficult to sell or trade in your vehicle without taking a financial hit.

Ultimately, the decision to finance should come down to your individual circumstances. Consider your income, savings, credit score, job stability, and future plans. Are you comfortable with a fixed monthly payment for several years? Can you afford a decent down payment? Would a used car or a smaller loan amount better suit your budget?

Financing can be a powerful tool, but like any financial decision, it requires careful thought. Don’t rush into a loan just because it’s offered. Take the time to weigh your options, run the numbers, and think long-term. If you do that, you’ll be in a much stronger position to decide whether financing truly fits your needs—or if another path, like leasing or saving up to buy outright, might serve you better.

Final Thoughts

Car financing isn’t as complicated as it might seem at first glance. Sure, it involves a few moving parts—credit scores, loan terms, interest rates—but once you understand the basics, it becomes much easier to navigate. The key is knowing how the process works and what lenders are actually looking for when they evaluate your application.

When you’re informed, you’re empowered. You’ll not only be able to avoid common pitfalls—like overextending your budget or locking into a high-interest loan—but you’ll also be able to spot better offers and negotiate with confidence. Whether you’re buying your very first car, upgrading to a newer model, or replacing a vehicle that’s seen better days, financing can give you the flexibility to choose something that truly fits your needs and lifestyle.

But remember, financing isn’t one-size-fits-all. What works for one person might not be right for another. That’s why it’s so important to take a step back before signing anything. Review your credit score, think about how much you can comfortably put down, and consider what monthly payment won’t stretch you too thin. Shop around, compare rates from different lenders, and don’t be afraid to ask questions—lots of them. A reputable lender will always be willing to walk you through the details.

At the end of the day, car financing is a tool—and like any tool, it works best when you use it with a clear plan. When you take the time to educate yourself and weigh your options, you’re far more likely to drive away not just with a car you love, but with a financing plan that makes sense for you long-term.

So if you’re thinking about financing your next vehicle, take a breath, do your homework, and move forward with clarity. The more informed you are, the better your chances of landing a deal that saves you money—and stress—down the road.

2 thoughts on “What Is Car Financing and How Does It Work?”

jfg9z6

pwb4ng